|

Hope of Israel Ministries (Ecclesia of YEHOVAH):

Massive Debt Bubbles Around the World Set to Burst

|

Right now, the U.S. has the financial strength to keep the European debt crisis from becoming catastrophic. However, if the U.S. comes face to face with an immediate financial crisis of its own -- as I think it will -- then all bets are off. When the U.S. can no longer help Europe, no boat is safe from sinking. |

by Robert Wiedemer

As long time investors know, there was once a point in time when you could invest in the U.S. and be relatively shielded from any economic chaos across the globe. Of course, when a rock was dropped into the U.S. pool, the ripples spread quickly worldwide, but that wasn't true in reverse. Like a sturdy battleship on the seas, the U.S. economy suffered nary a sway as rogue waves struck its hull.

But as the U.S. squandered its position as the world's largest economy and the U.S. dollar's status as its reserve currency, the ship was weakened. Economic storms battered the creaking boat, exposing cracks. Other countries grew in strength and stature, and the tentacles of the global economy further intertwined.

While the U.S. economy is still the world's largest, no longer is that size enough to protect and steady it, especially considering that mistakes of its own doing have not only set it off course but put the nation at the mercy of wary friends and foes alike.

As any global contrarian investor these days knows, no longer is the U.S. truly a safe haven for assets. But with an economic hurricane of epic proportions swirling nearly everywhere, where can one turn?

Europe is in constant and growing chaos. China, the growth engine of the post-recession world economy, is slowing down, as are many countries that export to China. Japan -- a nation rocked by natural disaster this year -- is troubled too, yet at least finds some solace in the signs its economy isn't declining as fast as many observers thought it would.

It's a wild world right now. To best understand it, we turn to two key areas. First, Europe, because it is the epicenter of a potentially deadly debt contagion, and then the economic ecosystem of countries that have leaned on China in the aftermath of the 2008 financial crisis -- countries that now face the prospects of a Chinese debt bubble about to burst.

The European Conundrum

Europe is facing two significant problems: 1) a slow recovery from the 2008-2009 recession and 2) a well-publicized debt crisis.

The debt crisis is in part related to the first problem. The lack of any significant recovery from the 2008-2009 recession in Spain, Greece, Ireland, Portugal and Italy is part of the reason their debt, which would be too large to handle even in "normal" circumstances, is much more obviously dangerous.

Given the current weak economies of these trouble spots, government austerity measures are only going to hurt those economies more. However, given that austerity is the primary way they will be able to pay off their debts, this doesn't leave government officials a lot of good options. The fundamental problem is that they never should have taken on so much debt in the first place, an issue obviously difficult to fix in hindsight -- the very slow-moving economies of these countries, with no viable economic engines to speak of, exacerbate the situation to a critical degree.

There are a large number of structural and bubble-related reasons for Europe's tepid recovery from recession. Many of these -- such as regulatory minefields stifling business output and expectations built into the social fabric stifling spending cuts -- are long-term problems that won't be solved quickly. However, the overriding problem that threatens Europe's economic future and the future of its stock markets and banking system in the most immediate sense is the debt crisis.

A Contagion Without Containment

Over the past few months, the European debt crisis has been spreading. Greece was the hot spot in late spring. Then in July the problems came to greater light in Italy, which holds the most government debt in relation to GDP of any eurozone nation, and Spain, which saw the interest rate demanded by investors for their 10-year bonds soar to over 6 percent.

Unfortunately, like a petulant child screaming for attention, Greece returned to the forefront of late. As investors attempt to dole out discipline -- yields on Greek one-year government debt have soared to a catastrophic 130 percent -- more and more the impetus has turned from staving off Greek default to trying to prepare for its imminent arrival.

The thing about Greece is, it's a relatively small country. And the world has been at this doorstep before, considering the country is a chronic defaulter. The real problem this time around is Greece's impact on investor confidence regarding Italy and Spain.

Greece, Portugal, Ireland and Spain in combination produce over one-third of the eurozone's gross domestic product. So if fear from a Greek default causes a dangerous domino effect, this is not a small problem.

As if this fire needed more fuel, France has been added as supercharged kindling. Rumors of a downgrade of French government debt are flying and major French banks, such as Societe Generale and Credit Agricole, have suffered stock price declines over 50 percent. Credit default swaps on French government bonds -- a form of insurance against bond default -- are now selling at the same price as CDS on Italian bonds were selling in June. The crisis is swelling beyond the scope of what Germany and a struggling European Union can handle.

When a Few Loans Go Bad, Blame The Borrowers; When a Lot of Loans Go Bad, Blame the Lenders

Of course, it takes two to play the debt game: one to borrow and another to lend. Who did a lot of lending to both public and private borrowers in Portugal, Greece, Ireland, Spain and Italy?

France and Germany, of course.

In fact, their public and private debt exposure to these countries amounts to over $1.6 trillion. Italy alone owes France $500 billion, which is equivalent to about 20 percent of France's GDP.

France is especially vulnerable because its own economy is not as strong as Germany's and is slowing rapidly. Growth in the French economy came to a complete halt in the second quarter of this year. Combine France's own dramatically slowing economy with its enormous exposure to other countries' falling economies that are heavily indebted, and you have a lender in very big trouble. The crisis of the borrowers has now spread to a crisis for the lenders, just as the housing crisis spread to the lenders in 2008 with disastrous consequences.

So far, Germany has remained above the fray, in part due to its very strong economy that has been supported by massive growth in exports to China. However, even Germany's economy has now stopped growing, in part due to a big slowdown in China's bubble economy. As Germany starts to struggle, it too will join the growing list of lenders in trouble.

The short-term solution to save the lenders from massive losses has been to print money to buy bonds. The European Central Bank recently began buying Italian and Spanish government bonds with printed money. That cheered both European and U. S. stock markets. The interest demanded for Spanish and Italian 10-year bonds quickly dropped into the mid 4 percent range from over 6 percent, although it has risen significantly since then.

The problem is that the short-term fix doesn't last forever. Eventually you get the future price tag of money printing: inflation.

Money printing is a shot of adrenaline for financial markets these days in the U.S. and around the world. However, money printing in Europe is more limited than in the U.S. because approval to bail out Greece, Italy, Spain, Ireland and Portugal has to come from France and Germany. France and Germany will be much more reluctant than the other countries to print money to save those countries. However, since the borrower's problem is also the lender's problem, the lenders (France and Germany) will be under pressure to save those countries so that they can save their own banks.

The Euro as Scapegoat

During this debt crisis, some analysts have viewed the currency -- the euro -- as a culprit. The idea of banding together such economically disparate countries under the umbrella of one currency was too unwieldy when you factor in the resulting inability of governments to respond to their own internal economic instabilities.

There's merit to that argument, but what we're facing isn't in my view a fundamental euro problem -- it's a fundamental debt problem.

This is an important distinction. France and Germany's interest in saving other countries in the eurozone is often portrayed as an attempt to save the euro. But their real interest is in saving French and German banks. Dropping the euro won't pay off the public and private debt they hold from those other countries. If Greece dropped the euro, and converted back to drachmas, it wouldn't pay off their debt.

Whether the debt is in euros or drachmas or any other currency, it's still a debt and the French and German banks need to have it paid off or they will go under. Remember, French banks' exposure to Italian debt alone amounts to over 20 percent of the French GDP. The problem is enormous. Don't be distracted by the euro when the issue is debt.

The U.S. Fed to the Rescue

Europe's problems are setting off a chain reaction of potential defaults and downgrades. That puts pressure on U.S. banks, as well as our stock and bond markets. If U.S. markets were strong, this wouldn't matter as much. But they are fragile and vulnerable to shocks, especially if the Federal Reserve isn't propping them up with more immediate money printing. This chain reaction to U.S. banks and markets could easily become highly damaging in the current market environment.

|

|

Hence, the Fed has already been helping Europe by opening a currency swaps window that allows European central banks to borrow from the Fed and then give that money to troubled private European banks. The Fed says this is a safe bet because it is lending only to other central banks.

Technically it is true that the money is going to central banks -- but the central banks are giving that money to private European banks to bail them out. So in a very real sense, our Federal Reserve is now bailing out European banks.

Why? Because the potential consequences to our stock and bond markets of not doing it could be disastrous. If the situation in Europe gets worse, the U.S. could print even more money to help mitigate the eurozone debt crisis and keep it from hurting our banks and stock and bond markets too much. We wouldn't be doing this to help out the Europeans, but to save our own banks and markets. Hence, what would at one time be unthinkable (the Federal Reserve helping enormously to bail out Europe) could become reality if the situation worsens. And given the fundamentals of the European debt crisis, it will.

This means that Europe can't fail completely until the U.S. starts to have significant financial problems. Right now, the U.S. has the financial strength to keep the European debt crisis from becoming catastrophic. However, if the U.S. comes face to face with an immediate financial crisis of its own -- as I think it will -- then all bets are off. When the U.S. can no longer help Europe, no boat is safe from sinking.

Another Debt Crisis? Look to China

What's the big difference between the coming Chinese debt crisis and the current European debt crisis? A lot more printed money.

China has used its virtual printing presses to dramatically stimulate its economy. China's government-controlled banks have been the conduit for this new money, loaning it primarily to state-owned companies and state and local governments for massive infrastructure and real estate projects.

These loans were made more to stimulate the economy than to make a profit. The Chinese were desperate. When exports collapsed in 2008, tens of millions of Chinese workers lost their jobs. The government felt it had to do something or another Tiananmen Square (only larger) was in the making.

So, the loan spigots were opened. In fact, Chinese banks loaned more money in the first quarter of 2009 than in all of 2008. The lending continued through 2010, although it has slowed somewhat in 2011.

The Chinese debt crisis will occur when this gigantic artificial stimulus by way of loan binge begins to hit the brick wall of borrowers' inability to pay. Since so many of these loans were bad right out of the starting gate, some are already starting to go bust. In fact, the government has already had to initiate a TARP-type bailout of some Chinese banks. That bailout, in relation to the size of the Chinese economy, is already bigger than the U.S.'s Troubled Asset Relief Program bailout. And, the bad loans are just beginning to pile up.

In this sense, the Chinese and U.S. economies share similarities. Money printing is being used and will continue to be used, to help the U.S. manage its rapidly growing, entitlement-fueled government debt. As I wrote in last month's issue, the government's debt is now a massive toxic asset that can never be repaid and represents a very large bad debt, much like what China is accumulating today.

|

Of course, managing to avoid default through the use of money creation doesn't come without costs: There really is no free lunch. For both the U.S. and China, high inflation is the end result of a lot of bad debt. China's official inflation rate has been rising steadily and has just gone over 6.5 percent. The real inflation rate is likely much higher. Sound familiar?

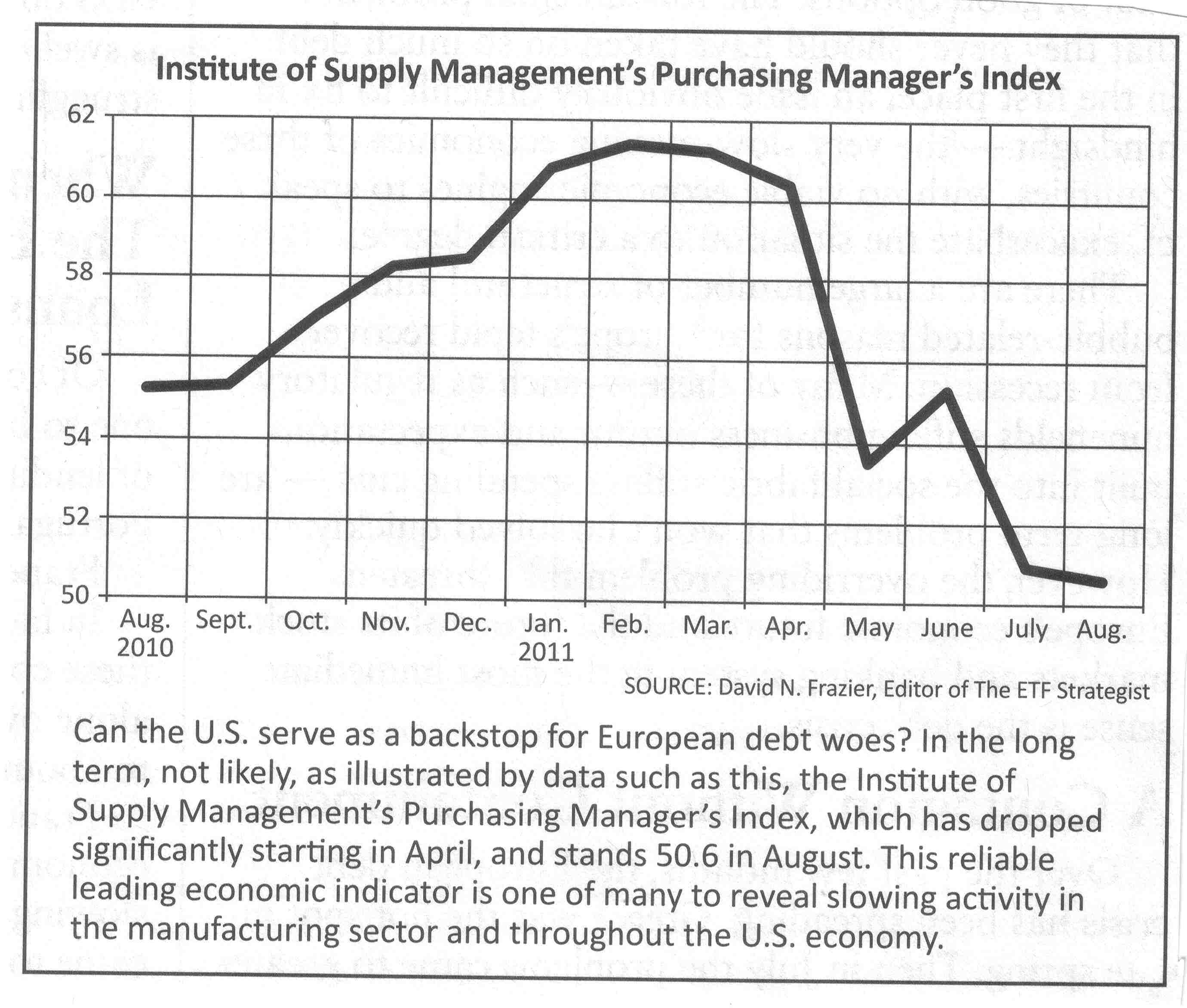

The threat of a Chinese recession raises the stakes. China is already showing signs of slowing growth. HSBC Bank's purchasing index for China has been falling and is close to negative. More telling is that the countries that export strongly to China are seeing economic growth come to a screeching halt or even decline. The recent slowdown in the economies of these supplier countries reveals much about the true state of China's economy.

Trouble Ahead for Australia, Brazil, Germany, Russia, Japan, and Others

Australia, which has benefited enormously from China's insatiable demand for natural resources, saw negative GDP growth in the first quarter of this year and very slow growth in the second quarter. Brazil and South Korea, both big suppliers to China, have seen their growth rates fall over 50 percent in 2011.

Even Canada is now experiencing negative job growth. To give you an idea of how much Canada has become more dependent on China, in 2010 China became Canada's number-one market for lumber exports, ahead of the United States. That's partly due to the decline in U.S. imports but it is also due to China's explosive growth in demand.

Finally, and perhaps most importantly, Germany, a huge supplier of machinery to China, experienced zero GDP growth in the second quarter of 2011. Germany's exports to China are a core reason it bounced back from the 2008-2009 recession and it has been the only viably strong economy in Europe.

Now, I'm not sure that the big slowdown in all these supplier countries to China indicates the popping of the Chinese construction bubble. But there is no doubt that it's beginning. The eventual pop will have far-reaching ramifications for the supplier countries' economies and stock markets.

It will also negatively affect the U.S. economy and stock market. After the 2008-2009 recession, there was little growth in Europe, Japan, or the U.S. These were the key drivers of growth in the past. After the recession, the whole world looked to China for growth. And China provided a lot of it, helping to power many emerging market countries, such as Brazil, as well as big commodity exporting countries, such as Australia and Canada. No surprise that big cities in both of those countries, such as Sydney, Vancouver and Toronto, had huge housing booms over the past two years.

Even economies that are not as directly supported by China will feel its effects. China's impact on commodities prices over the past few years has been enormous. Almost the entire increase in demand for oil over the past five years has been driven by China and those countries supporting its growth. If China's economy slows dramatically, the demand for oil will slow with it, pressuring Russia and the Middle East.

Another very important country affected by China will be Japan. Although it is not as dependent for its growth on China as are same emerging market or commodity producing nations, it uses China as a huge low-cost provider of many of the goods it sells to the U.S. and Europe. It also has significant trade with China. Japan's economy is already reeling from the earthquake and low demand for its products in Europe and the U. S. It will be particularly vulnerable to another blow from a faltering Chinese economy.

South Korea also falls into this category of a country whose growth is slowing, and it cannot afford a big decline in the Chinese economy. The country is feeling greater unease about its economy all the time. (Maybe that's a reason the Korean version of my book Aftershock has become a bestseller. If sales of Aftershock are any sign of the economic mood of a country, I should add that a Chinese publisher just bought the rights to the second edition of the book there.)

Psyched Out by Fading Growth

The bottom line is that the economies of many growing and developing nations have become increasingly dependent on China for growth. When the Chinese economy is in trouble, it will affect all of them. More importantly, it will affect stock market psychology around the world, which in some ways is more fragile than the world economy.

This slowdown in China and its effect on other Asian economies will provide headwinds to Asian stock markets, which will inevitably magnify the problems that stock markets in Europe and the U.S. are having due to their own issues.

Of course, as always, a shot of printed money by the Fed this autumn, while it won't turn the world economy around, could bolster many stock markets.

Yet, if such "quantitative easing" occurs, just like earlier money-printing efforts, the effects will be short term. And, eventually, the long-range effect in the form of runaway inflation will begin to threaten our economy and world stock markets like no other financial contagion we've seen before.

|

Hope of Israel Ministries -- Proclaiming the Good News of the Soon-Coming Kingdom of YEHOVAH God On This Earth! |

|

Hope of Israel Ministries |

|

Scan with your Smartphone for more information |